How to Apply for Aid

How to Apply for Aid

The cost of an education at the School of the Art Institute of Chicago includes more than just tuition—on this section of the site you’ll find a full breakdown, including housing, insurance, and more.

Some types of financial assistance are limited in funding, so the earlier you apply, the better. SAIC begins issuing financial aid awards for eligible students in January each year.

Helpful Tools from Federal Student Aid

Federal Student Aid Estimator: Federal Student Aid has a Federal Student Aid Estimator that provides an estimate of how much federal student aid the student may be eligible to receive. These estimates are based on the Student Aid Index (SAI), an index number used to determine federal student aid eligibility.

Parent Wizard: Federal Student Aid provides the Parent Wizard Tool to help students and families determine who will need to provide contributor information on the 2025-26 FAFSA prior to starting the form.

ISAC Raising Awareness/2025-26 FAFSA Updates: The Illinois Student Assistance Commission (ISAC) is the trusted source of college planning information for Illinois students and their parents. ISAC will communicate additional updates to students and parents once the new FAFSA becomes widely available to everyone each year. If you have not done so, be sure to sign up for ISAC's e-Messaging service to receive important updates and reminders throughout the year.

Financial Aid Next Steps

-

In order to be eligible for need-based aid every year such as SAIC, state and federal grants, loans and work study, as well as non-need-based federal loans, eligible students need to file the Free Application for Federal Student Aid (FAFSA) at fafsa.gov which opens every year on October 1 before the new academic year.

Priority Deadline to submit the FAFSA:

Fall 2025 (2025-26): January 1, 2025

Fall 2026 (2026-27): January 1, 2026Helpful Tips

- Three to five days after you file your online FAFSA, you will be emailed a confirmation. Review your processed FAFSA carefully to ensure that you have supplied the correct data and follow any further instructions

- There may be questions you need to answer based on information you provided on the FAFSA. We will contact you by postal mail and email if we need clarification or additional documentation. Please respond as soon as you receive this request to avoid any delay in processing your financial aid. Items are also listed in Self-Service under the "Tasks" tile.

- If you feel the FAFSA has not accurately represented your financial situation, or there has been a change in family finances—loss of employment, separation, divorce or death, for example—you may need to submit a Professional Judgement Financial Aid Appeal.

Merit Scholarships

Admitted students are reviewed for SAIC's merit-based scholarship (based on a holistic review of your application and not on need) once you have been admitted to SAIC. No additional paperwork or applications are necessary. See additional merit scholarship info.

Outside Scholarships

We recommend searching sources like fastweb.com or speaking with your high school or college counselor about other local scholarship opportunities. Also consider scholarships offered by any professional, community, or religious organization of which you are a member. See additional outside scholarship sources and information.

International Student Financial Aid

International students are not eligible to complete a FAFSA. Institutional merit scholarships are determined at the time of admissions. Details on international student financial assistance resources are available on the International Funding Resource section of our website.

-

An official Financial Aid Award Offer notification email outlining your financial aid offer will be sent to you once your file has been reviewed and your eligibility has been determined. You can then view your financial aid award offer in Self-Service. Newly admitted students, who complete a FAFSA, will also receive a Financial Aid Award Offer Packet by way or U.S. mail to your home mailing address.

-

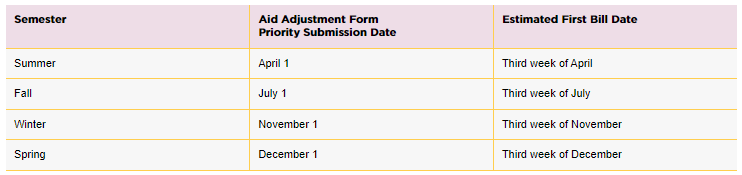

At SAIC, tuition and financial aid are calculated per credit hour. If you decide to enroll in something other than the standard enrollment for your program (for example, 15 credits/semester for undergraduates in fall or spring) notify SFS immediately by submitting an online Early Aid Actual Adjustment Form by the dates below so your aid can be calculated to match your enrollment. This will ensure more accurate invoices and statements. By submitting this form, SFS staff will update your award on Self-Service and notify you by email.

-

Use these electronic Figure Your Cost Budgeting Worksheets to calculate your direct and indirect costs each semester. Direct costs are costs for which you will be billed by SAIC directly on the student's tuition and fees account. Indirect costs are costs for which you will need to budget, but will not be charged by SAIC.

-

The School of the Art Institute of Chicago (SAIC) administers several loan programs to help ensure that all eligible admitted students are able to cover the cost of tuition. Eligibility for federal programs is based on the results of the Free Application for Federal Student Aid (FAFSA) application. Information on each type of loan, interest rates and fees can be seen on SAIC's Student Loan section of the website.

In order to accept and secure the Federal Stafford loans that they have been offered, first-time student borrowers must complete two loan steps, generally just one time at SAIC. The Federal Direct PLUS and Private loan programs also require that the borrower is creditworthy or has a creditworthy endorser (a co-signer). All loan steps should be completed by July 1 before each fall-to-spring academic year and by January 1 for spring-only semesters. Borrowers must reapply for Federal Direct PLUS and private loans each year or term that the loan is desired.

Please see here for information regarding the loan steps that must be completed in order to secure these loans.

-

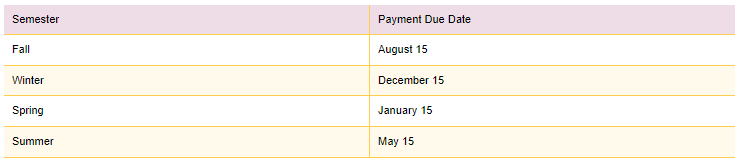

Payment in full or payment arrangements of any balance not covered by financial aid (including loans) must be made by the following dates in order to avoid late fees, restriction of access on campus, and prevention from future registration and release of diplomas:

Suggested Priority Deadlines

2026–27 Award Year (beginning with summer 2026)

- February 1, 2026, for undergraduate Illinois residents (due to State Aid deadlines)

- March 1, 2026, for all other students.

Free Application for Federal Student Aid (FAFSA)

Available October 1 before each school year

To apply for federal and state aid, as well as SAIC's need-based aid, students must complete the Free Application for Federal Student Aid (FAFSA) each year. Students and parents should work together to complete the FAFSA at fafsa.gov.

You can:

- Learn how to fill out the FAFSA.

- View state deadlines.

- Learn who is eligible for aid.

- Complete the Free Application for Federal Student Aid (FAFSA) to apply for financial aid for college or grad school. Once the FAFSA is submitted online, SAIC will receive an electronic copy from the federal government, as long as the school code (001753) was included.

- Learn when and how your aid will be paid out.

- Make corrections to your FAFSA: Review and submit corrections within five days to ensure accurate financial aid estimates.

Helpful Information and Tools

Your FAFSA ID: You and Contributors (if applicable) Digital Signature

You and your contributors (such as parents and/or spouses, if applicable) will need an FSA ID to sign your FAFSA. It is your digital signature used for signing the FAFSA each year, as well as loan applications, online counseling sessions, and other financial aid documents. You can also use it to access your financial history and information at StudentAid.gov.

Student Aid Index (SAI)

The FAFSA collects information about the student (and parents for dependent students) regarding income, the number of family members, and assets and determines a level of financial need for the student. SAIC uses the resulting Student Aid Index (SAI) as part of a formula to determine the amount of financial assistance to be provided to the student for their education.

After You Complete the FAFSA

SAIC will receive an electronic copy of your FAFSA for processing (remember to list SAIC's school code 001753) once you have submitted. You will receive an email confirmation that your FAFSA has been processed within 5 days. You must review and submit any corrections at fafsa.gov within five days to ensure accurate financial aid estimates.

All degree-seeking students will be sent an official Award Letter packet outlining financial aid options and the next steps required in the process. Typically, the award is based on full-time enrollment/standard enrollment for the program; any deviation from that condition will, most likely, result in a change in the financial aid award and requires notification from the student to Student Financial Services. Most aid sources require the student to be enrolled at least half-time. See the Adjusting Your Aid for Enrollment page for additional details.

If you need to make corrections to your FAFSA they should be made within five days to ensure accurate financial aid estimates.

Students who would like a financial aid offer, including merit scholarships, for summer and winter terms must complete a SAIC application and an annual FAFSA for federal financial aid (if eligible). See saic.edu/summerwinterfa for additional information.

Upon awarding financial aid eligibility, students are notified by email for on-campus classes and email for study trips. Students can view their financial aid in their Self-Service account. Updates to award offers are also sent by email.

Criteria for Continued Eligibility

To continue receiving financial aid, you must make financial aid satisfactory academic progress (FASAP) by maintaining a minimum GPA and completing a set percentage of courses, be enrolled in an eligible program at an eligible school, maintain your status as an eligible student, avoid financial default, and annually submit the FAFSA form. Schools establish their specific SAP policies, which often involve a financial aid warning or probation period if standards are not met.

Financial Aid Satisfactory Academic Progress (FASAP): You must meet SAIC's financial aid standards for academic progress known as FASAP, including getting credit in a specific number of credit hours attempted and completing a required percentage of attempted coursework to stay on track, known as Pace, for your degree. Please note this is different from the SAIC academic standards for academic progress.

- You must remain enrolled as a regular degree seeking student in an eligible degree or certificate program at SAIC. Courses taken that are not needed for the student's degree requirements may not receive federal, state or institutional financial aid.

- You must file the Free Application for Federal Student Aid (FAFSA) (or its equivalent) each year to determine your continued financial need and eligibility.

Financial Aid Forms

Forms such as student budgeting worksheets, federal verificaiton, etc. Visit Forms and Guides for more information.